In 2024, the real estate industry went through one of the biggest shake-ups in decades. Class-action lawsuits and the National Association of REALTORS® (NAR) settlement made national headlines, sparking questions about how real estate agents are paid and whether commissions would finally go down.

Why all the attention? For years, the traditional structure was that sellers offered compensation to the buyer’s agent. This offer of compensation was published in the MLS, so both agents could see it. To most buyers, it felt like working with an agent was “free” because they didn’t see a separate bill. In reality, the seller was paying both sides through the proceeds of the sale.

Lawsuits argued that this system was anti-competitive, kept commissions artificially high, and wasn’t fully transparent to consumers. When the settlement was announced, the assumption was clear: broker fees were about to change in a big way.

What Changed in 2024

Several new rules went into effect:

- MLSs no longer display buyer broker compensation.

- Buyers must sign written agreements with their agent before touring homes. This spells out exactly how their agent is paid.

- Sellers can still offer buyer broker compensation, but it is now treated as a negotiable term in the purchase contract instead of being advertised in the MLS.

What Actually Happened

Here’s where it gets interesting. Depending on which numbers you look at, the story sounds a little different.

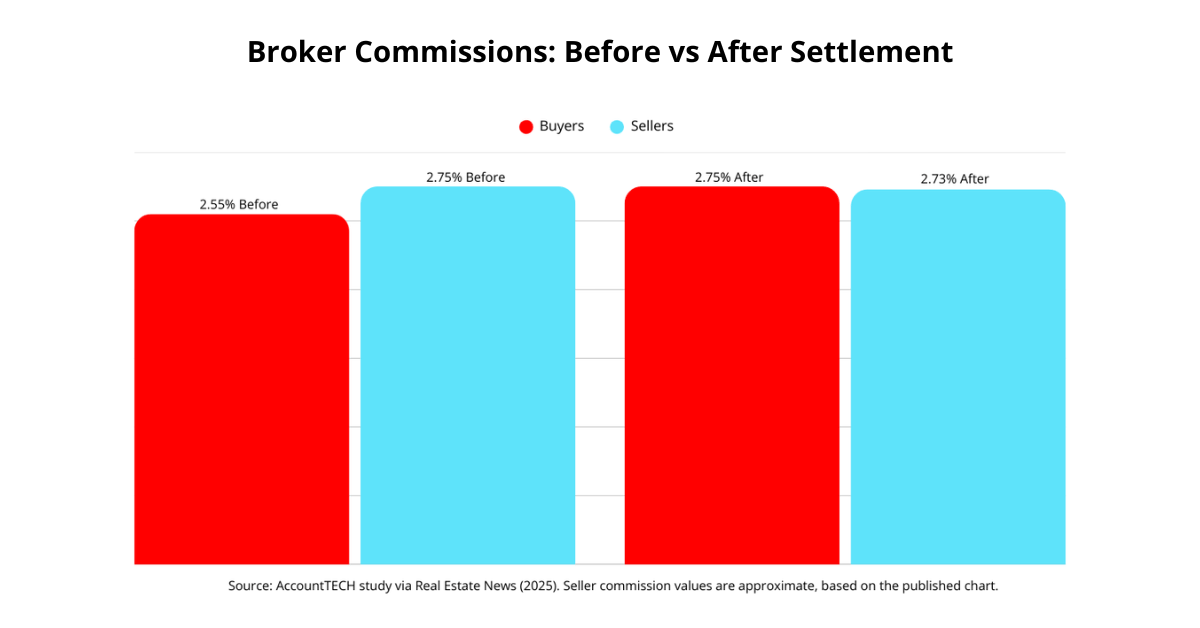

News coverage summarized the change by saying buyer commissions rose only slightly, from around 2.50% before the settlement to 2.55% a few months later, while seller commissions slipped from about 2.80% down to 2.73%.

But the actual AccountTECH study of more than 224,000 transactions, as published in Real Estate News, shows a bit more detail. According to their chart, buyer commissions were already closer to 2.55% just before the settlement. After dipping briefly, they rebounded and climbed to nearly 2.75% by January 2025, five months after the new rules took effect. Seller commissions, on the other hand, eased back only slightly, from about 2.75% pre-settlement to around 2.73%.

The takeaway? Commissions did not collapse. If anything, the numbers suggest stability, and in the case of buyers even an increase, which reinforces the idea that consumers continue to place value on having professional representation during one of the most significant financial transactions of their lives.

What This Means for Buyers and Sellers

So why are we still talking about this? Because while the cost hasn’t shifted much, the process has changed.

- Buyers are now more aware of what they’re signing when they hire an agent, because the agreement is written and up front.

- Sellers are still often offering compensation, because it makes their property more appealing to buyers who may already be stretched financially.

- Negotiating broker fees is now a more visible part of the deal, which can sometimes create tension, but it also means everyone is clearer about who pays what.

Why Value Still Matters

At the end of the day, these numbers show that commissions have remained stable and, for buyer agents, even increased. That tells us something important: consumers continue to place value on working with a trusted professional during one of the biggest financial decisions of their lives.

Real estate is not just about contracts and percentages. It is about guidance, strategy, and support from start to finish. The settlement may have changed how fees are displayed, but it has not changed the fact that people want an expert on their side when they buy or sell a home.

If you are thinking about a move in Downers Grove, DuPage County, or anywhere in the Western Suburbs, The Tully Team at Platinum Partners Realtors is here to help. Visit The Tully Team to explore our resources or connect directly to talk about your plans. If you would like details on how these rule changes impact both buyers and sellers, you can request those resources on our website as well.

References

Disclaimer: This content is provided for general information only and reflects published third-party research. It should not be taken as financial, legal, or tax advice. Always consult the appropriate professional for guidance on your specific situation.

Commission rates are not fixed. They are always negotiable and can vary depending on the market, the property, and individual client circumstances.